SEBI’s 3% Exit Load Rule: Critical Risk Every Investor Must Know

When I first read the latest circular from the SEBI-Securities and Exchange Board of India, I immediately realised this wasn’t just another routine regulatory tweak. It signalled a deeper push toward reshaping investor behaviour, especially for those entering the newly introduced Life Cycle Funds category. And honestly, after analysing the details, I think this move says more about investor psychology than it does about fees.

Table of Contents

ToggleAs someone who closely tracks policy changes that affect personal portfolios, I always look beyond headlines. The recent recategorisation update introduces a structured exit load framework specifically for Life Cycle Funds. At first glance, it looks like a simple fee rule. But when I examined it closely, it became clear that the regulator is intentionally nudging investors toward long-term discipline.

In this article, I break down the new exit load rule for Life Cycle Funds, explain why it was introduced, who it impacts the most, and what it means for investors like us in practical terms. I’ll also share my personal interpretation of the change, how it fits into the regulator’s broader strategy, and whether it should actually influence your investment decisions.

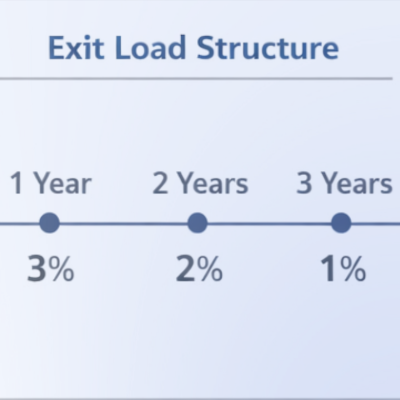

What Exactly Has Changed?

Under the new rule, Life Cycle Funds now carry a graded exit load structure:

- 3% exit load if you withdraw within 1 year

- 2% exit load if you withdraw within 2 years

- 1% exit load if you withdraw within 3 years

- No exit load after 3 years (unless scheme documents specify otherwise)

Importantly, this rule only applies to Life Cycle Funds. If you hold equity, debt, or hybrid mutual funds, nothing changes for you right now.

When I compared this with existing mutual fund exit load structures, I noticed that most funds typically have either a flat short-term exit load or none at all. A graded structure like this is unusual, and that’s precisely why it caught my attention.

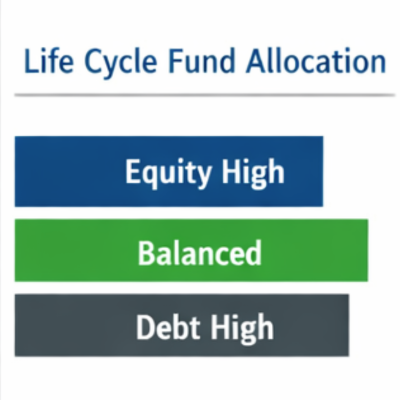

What Are Life Cycle Funds And Why SEBI Is Focusing on Them

Life Cycle Funds are designed as goal-based investment vehicles with a defined maturity timeline. Their structure follows a glide-path approach:

- Early years: higher equity allocation

- Mid phase: balanced allocation

- Later years: higher debt allocation

In simple terms, these funds automatically reduce risk as you approach your financial goal, whether that’s retirement, a child’s education, or long-term wealth creation.

From a design standpoint, these products only work well if investors stay invested for most of the cycle. Frequent withdrawals would defeat the entire purpose. That’s exactly why the regulator stepped in.

Why This Rule Makes Sense to Me

When I look at investor behaviour patterns, especially among retail investors, one trend stands out: many people panic during market volatility and exit too early. This often leads to buying high and selling low, the opposite of successful investing.

By introducing a declining exit load, the regulator is essentially saying: “If you commit to a long-term product, stay committed.” And honestly, I think that’s a fair message. This isn’t a punishment. It’s a behavioural nudge.

Exit Load: A Quick Practical Example

Whenever I explain exit loads to new investors, I use a simple illustration:

If I invest ₹1,00,000 and redeem within one year when a 3% exit load applies:

- Exit load deducted: ₹3,000

- Amount received: ₹97,000 (before market gains/losses)

This deduction happens automatically at redemption. It’s not billed separately, which is why many investors overlook it.

How This Affects Different Types of Investors

After reviewing the structure, I realised the impact depends entirely on your investing style.

- Long-Term Investors, Almost No Impact: If you plan to stay invested for 3+ years, this rule won’t bother you at all. In fact, it may even protect you by discouraging impulsive decisions.

- Short-Term Investors, This Is a Warning Sign: If you tend to invest money you might need soon, Life Cycle Funds may not be suitable anymore. The cost of early exit is now clearly defined.

- Goal-Based Planners, Positive Development: For investors who actually use funds for planned goals, this structure strengthens the product’s purpose.

Personally, I see this as SEBI trying to match product design with investor intent, something that hasn’t always happened in the mutual fund industry.

Also Read: Technology Funds Drop in IT Rout 2026

The Bigger Picture, SEBI’s Strategy

This rule didn’t come in isolation. It’s part of a broader mutual fund recategorisation exercise that includes:

- Introducing Life Cycle Funds as a new category

- Phasing out the old solution-oriented category

- Standardising structures across fund houses

When regulators refine categories, they’re usually trying to solve a systemic issue. In this case, that issue appears to be misaligned expectations, investors treating long-term funds like short-term parking tools.

What I Think Investors Should Do Now

Whenever regulation changes, I ask myself one question: “Does this change how I should invest?”

For Life Cycle Funds, here’s the checklist I’d personally follow before investing:

- Confirm my investment horizon is at least 3+ years

- Ensure I won’t need liquidity early

- Read the Scheme Information Document carefully

- Understand the glide-path allocation strategy

If I can’t tick all four boxes, I’d reconsider investing in this category.

My Honest Take: Is This Good or Bad?

After analysing the circular, I don’t see this as restrictive. I see it as clarifying. For years, many investors entered long-term products without fully understanding commitment periods. This rule makes expectations explicit.

Transparency is always good for markets. And in my view, that’s what this change really delivers. If you choose a Life Cycle Fund, treat it like a long-term contract with your future self, not a short-term trade. That’s the mindset this new rule is trying to enforce.

Final Thoughts

Regulatory updates often sound technical, but they usually reflect a deeper philosophy. In this case, the message is clear: investing success comes from patience, not timing.

And if a small exit load helps investors stay disciplined and reach their goals, it might actually be one of the most investor-friendly rules introduced in recent years.

Also Read: Mutual Funds: 5 Powerful Tax Rules to Avoid Losses

Disclaimer

This article reflects personal analysis and interpretation for educational purposes only. It is not investment advice. Mutual fund investments are subject to market risks. Always consult a SEBI-registered financial advisor before making investment decisions.