When Oracle shares plunged roughly 11% after earnings, it wasn’t because the company was failing. In fact, demand for its AI infrastructure is booming. The trigger was something far more subtle: revenue that missed expectations.

The company reported quarterly revenue of $16.06 billion, slightly below analyst estimates of $16.21 billion (compiled by LSEG). That gap may look small on paper, but in markets, expectations are everything. From experience, I’ve learned that stocks rarely fall because numbers are bad; they fall because numbers aren’t good enough.

In this article, I will break down why Oracle’s shares fell despite strong AI demand, what triggered the broader decline in AI-linked stocks, and whether the market reaction reflects deeper concerns about growth, debt, and cash flow, or simply short-term sentiment.

The Ripple Effect Across AI Stocks

The moment Oracle slipped, I noticed another familiar pattern: sympathy selling.

- NVIDIA fell about 1.5%

- Micron dropped around 2%

- CoreWeave slipped close to 1%

This is classic market psychology. When one major AI infrastructure player disappoints, investors briefly question the entire sector’s valuation.

I’ve seen this playbook before, whether during cloud hype cycles, EV rallies, or fintech booms. Momentum sectors move together, especially when sentiment shifts.

The Debt Question Investors Can’t Ignore

One thing I’ve personally been tracking for months is Oracle’s aggressive capital spending.

After raising $18 billion through a massive bond sale, one of tech’s largest companies doubled down on infrastructure. It’s building data centres and expanding capacity to compete directly with hyperscalers like:

- Amazon

- Microsoft

That’s a bold move. But bold moves often come with debt. According to analyst Tyler Radke from Citi, Oracle may raise $20–30 billion annually over the next three years to fund expansion.

As an investor, this is the part I pay close attention to, not just growth, but how that growth is financed.

Management’s Defense, And Why It Matters

During the earnings call, CFO Doug Kehring reassured investors that Oracle intends to maintain its investment-grade rating. He also highlighted alternative financing methods:

- Customers installing their own chips in Oracle data centres

- Suppliers leasing hardware instead of selling

This is actually a clever strategy. It aligns payments with revenue inflows, reducing borrowing pressure. When I hear management talk about cash-flow synchronisation, that’s a signal they understand investor concerns.

The Capex Surge and Cash Flow Reality

Oracle now expects about $50 billion in capital expenditure for the full year, up sharply from $35 billion projected earlier.

But here’s the number that made investors nervous: Free cash flow for the November quarter was $10 billion, and the expected amount is about $5.2 billion

Negative cash flow in a high-growth phase isn’t unusual. Still, markets dislike surprises, especially negative ones.

Why Analysts Aren’t Panicking

Despite the sell-off, analysts at Wedbush Securities called this a “high-class problem.” Their reasoning resonates with me:

- AI demand is real

- Oracle’s backlog is strong

- Infrastructure expansion suggests long-term growth

In other words, the drop may reflect short-term expectations, not long-term fundamentals.

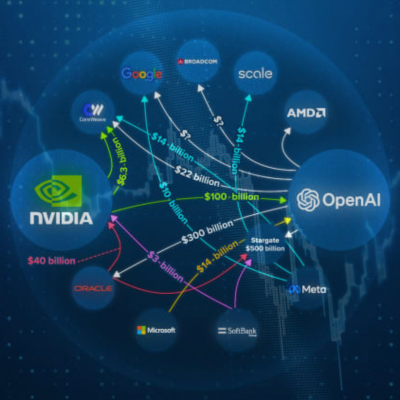

The $300 Billion Catalyst Few Are Talking About

One development that keeps Oracle on my watchlist is its massive deal with OpenAI, reportedly worth up to $300 billion.

That kind of contract doesn’t happen unless a company is seen as a serious infrastructure contender. When markets panic about quarterly numbers, they sometimes overlook structural shifts like this. And in my investing journey, those overlooked shifts are where opportunity usually hides.

My Interpretation as an Investor

Here’s how I personally break down situations like this:

- Short-term view: Revenue miss leads to sentiment drop and stock fall.

- Medium-term view: Heavy spending leads to weaker cash flow and investor caution.

- Long-term view: AI demand combined with infrastructure scale suggests potential upside.

Markets tend to focus on the first two. I try to spend more time analyzing the third.

A Pattern I’ve Seen Repeatedly

This isn’t the first time a tech company sold off after investing heavily ahead of demand. Historically:

- Cloud leaders spent years posting thin margins before dominating.

- Semiconductor giants invested billions before AI demand exploded.

The lesson? Markets often punish companies for investing before the payoff arrives.

Also Read: AI stocks Fall For A Third Day As Oracle And Nvidia Drop.

Why the Stock Is Still Up 34% This Year

Even after the drop, Oracle shares remain about 34% higher year-to-date.

That tells me something important: Investors still believe in the long-term AI infrastructure story. Temporary declines inside strong uptrends are common. In fact, they often act as reset points rather than trend reversals.

Key Takeaways I’m Watching Closely

If you’re tracking Oracle like I am, these are the metrics worth monitoring:

- Free cash flow trend over the next two quarters

- Debt levels vs revenue growth

- New AI infrastructure contracts

- Data center utilization rates

Those will tell us whether the current sell-off was justified or an overreaction.

Final Thought, My Honest View

Personally, I don’t see this as a crisis for Oracle. I see it as a test.

The company is essentially betting tens of billions that AI infrastructure demand will explode, and it’s building capacity ahead of that curve. That’s risky, yes. But transformative opportunities usually are. Sometimes the market punishes ambition before rewarding it.

Also Read: Adani Wipeout Fails to Break Foreign Investor Trust

Disclaimer

This article is for informational and educational purposes only and should not be considered financial advice. Investing in stocks involves risk, and readers should conduct their own research or consult a qualified financial advisor before making investment decisions.