When I first read about the RBI MPC Repo Rate decision, my immediate reaction was simple: nothing has changed again. But the more I sat with it, the more I realised that sometimes, no change is actually a decision worth paying attention to.

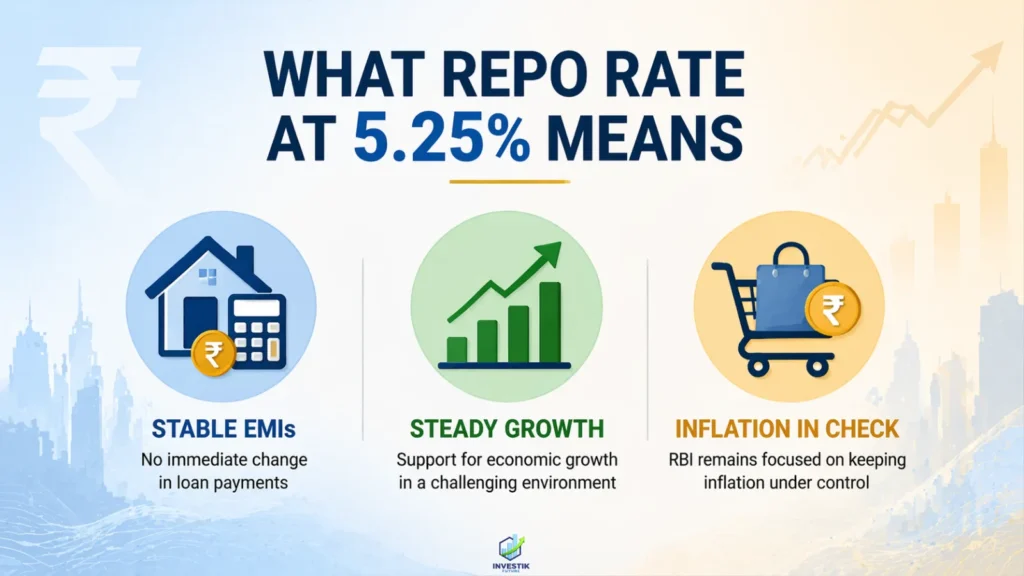

On April 8, the Monetary Policy Committee (MPC) unanimously decided to keep the repo rate unchanged at 5.25%. This comes after a similar pause in February, and honestly, it feels like the RBI is deliberately choosing stability over experimentation right now. As someone still trying to fully understand how macroeconomics plays out in real life, I see this move less as “boring policy” and more as a signal: the central bank is watching, waiting, and not ready to act yet.

This article reflects on the Reserve Bank of India’s decision to keep the repo rate unchanged at 5.25%. It highlights how the Monetary Policy Committee is prioritising stability amid global uncertainties, while also noting slight concerns like a revised lower GDP growth forecast (6.9% for FY27) and moderately elevated inflation (4.6%). Overall, this is a piece that reads as interpreting the policy as one of “wait-and-watch,” and examines what this means for everyday people and new investors.

Why is the RBI MPC repo rate unchanged?

As of now, it seems the RBI is balancing growth and inflation. The repo rate staying at 5.25% means:

- Borrowing costs remain unchanged

- EMIs won’t suddenly spike

- Liquidity conditions stay stable

Along with this:

- Standing Deposit Facility (SDF): 5%

- Marginal Standing Facility (MSF) & Bank Rate: 5.5%

Even the policy stance remains ‘neutral’, which I interpret as that we’re not committing to cuts or hikes yet.

The GDP Revision: A Slight Reality Check

This is where it started to feel more real for me. RBI now estimates India’s GDP at 6.9% in FY27, down from an estimate of 7.4% for FY26.

A 6.9% rate still looks good at first glance. But then I paused at the downward revision. Seems like the RBI is softly admitting that growth may not be as easy from now on.

Quarter-wise, the revisions look like this:

- Q1 FY27: 6.8% (slightly lower)

- Q2 FY27: 6.9% (slightly higher)

What I take from this is that growth isn’t collapsing, but it’s definitely not accelerating either.

Inflation Outlook: Still Under Watch

Inflation is something I personally feel more than I understand, especially when grocery bills go up. The RBI now expects inflation for FY27 at 4.6%, which is slightly above its comfort target of 4%.

Here’s what changed:

- Q1 inflation: revised up to 4.4%

- Q2 inflation: revised down to 4%

This is also the first inflation forecast based on the new CPI series released in February, which makes it even more interesting. To me, this is an indicator that inflation is not out of control, but also not completely settled.

Also Read: RBI MPC 2026: Rising Risks Drive Cautious Policy Outlook

How I’m Looking at This Right Now

Here’s how I see this decision:

- Loan EMIs Stay Predictable: If you are paying EMIs (or planning to), this pause is a relief. No sudden surprises.

- Markets Might Stay Range-Bound: Since there’s no significant policy change, I am not expecting a major market response immediately.

- Wait-and-Watch Phase Continues: This is perhaps the most important key point. RBI isn’t in a hurry, and perhaps investors shouldn’t be either.

The Bigger Picture: Why This Pause Feels Important

The more I consider it, the more I think this isn’t merely a “no change” policy. It’s a signal of caution. Amid global uncertainties such as geopolitical tensions and volatile crude oil prices, the RBI appears to be saying: “We would rather wait for clarity than act too soon.” And to be frank, it seems like a practical strategy.

My Personal Takeaway

To summarise this policy in one line, it is: “Stability over action.” As a learner myself, I’m actually reassured by this. It allows me to formulate thoughts around trends instead of responding to material changes.

At the same time, the minor downgrade in GDP and persistent inflation signals serve as a reminder that things are not entirely smooth either. So for now, I’m choosing to:

- Stay cautious

- Avoid overreacting

- Keep learning

Also Read: RBI NRI Deposits Plan: Can It Save Falling Rupee?

Frequently Asked Questions (FAQs)

1. What is the repo rate, and why does it matter?

The repo rate is the rate at which banks borrow money from the RBI. The RBI drops interest rates, EMIs & general liquidity in the economy directly by doing so.

2. Why did the RBI keep the repo rate unchanged?

Due to global uncertainties, manageable inflation levels and the need to support steady economic growth, the RBI preferred stability.

3. How does this decision affect common people?

It maintains loan EMIs, prevents abrupt borrowing cost shifts, and establishes predictable financial conditions.

4. Is 6.9% GDP growth good for India?

Yes, it’s still relatively strong globally, but the downward revision points to growth possibly easing a little now.

5. What should investors do after this policy?

You don’t have to do anything drastic at this time. In such relatively stable policy environments, a more cautious, long-term approach works best.

Disclaimer

This article is not intended to give investment advice. None of the above should be construed as financial or investment advice. Readers are requested to do their own research or consult a qualified investment advisor before making any investment decisions.

Himani Soni

I’m Himani Soni, a finance content strategist with 2+ years at Investik Future. I decode market trends and simplify complex investing concepts into clear, actionable insights for the everyday investor.